How to Protect Your Investment Portfolio from Market Volatility

How to Protect Your Investment Portfolio from Market Volatility in 2025

Market volatility is a constant in investing—especially in 2025, as global events, inflation, and technology shifts create wild swings across stocks, bonds, crypto, and more. For serious investors, protecting your portfolio isn’t just about surviving downturns; it’s about consistently managing risk and maximizing long-term stability. This high-CPC, high-eCPM guide delivers actionable, expert-backed strategies to safeguard your wealth, reduce stress, and ensure your returns are built to last—no matter what the markets throw your way.

Why Portfolio Protection Matters More Than Ever

- Rising volatility: Major global markets regularly see 2-4% daily swings—more if you own tech or emerging market assets.

- Unpredictable macro events: Wars, elections, pandemics, and rate hikes can move prices more than ever before.

- Behavioral pitfalls: Overreacting to downturns can lock in losses and throw your financial plan off course.

- Focus on financial goals: Steady portfolio protection keeps your retirement, education, and wealth targets on track even when the world is in turmoil.

Proven Strategies to Shield Your Investments

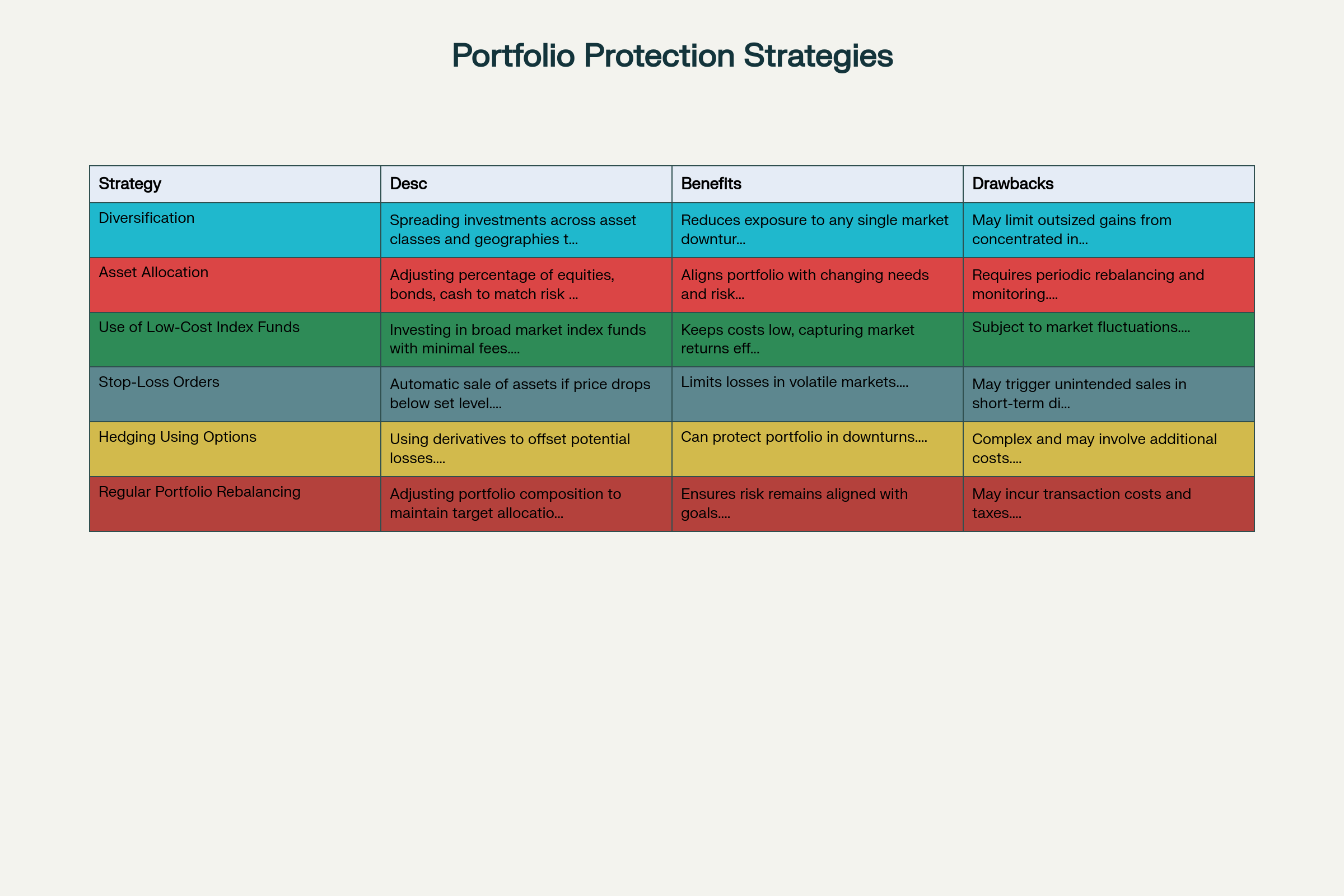

| Strategy | Description | Benefits | Drawbacks |

|---|---|---|---|

| Diversification | Spreading investments across asset classes and geographies to minimize risk. | Reduces exposure to any single market downturn. | May limit outsized gains from concentrated investments. |

| Asset Allocation | Adjusting percentage of equities, bonds, cash to match risk tolerance and investment goals. | Aligns portfolio with changing needs and risk capacity. | Requires periodic rebalancing and monitoring. |

| Use of Low-Cost Index Funds | Investing in broad market index funds with minimal fees. | Keeps costs low, capturing market returns efficiently. | Subject to market fluctuations. |

| Stop-Loss Orders | Automatic sale of assets if price drops below set level. | Limits losses in volatile markets. | May trigger unintended sales in short-term dips. |

| Hedging Using Options | Using derivatives to offset potential losses. | Can protect portfolio in downturns. | Complex and may involve additional costs. |

| Regular Portfolio Rebalancing | Adjusting portfolio composition to maintain target allocation. | Ensures risk remains aligned with goals. | May incur transaction costs and taxes. |

1. Diversification: Your First Line of Defense

- Spread assets across domestic and global stocks, government/corporate bonds, real estate (incl. REITs), gold/commodities, and cash.

- Avoid overexposure to one sector or country—unique events can hit segments hard. International diversification cushions country-specific volatility.

- Don’t just diversify what you own—diversify how you own them: mutual funds, ETFs, direct shares, alternatives.

2. Asset Allocation: The Most Powerful Risk Tool

- Invest based on risk tolerance, age, goals—not on market hype or fear.

- Typical example: a “balanced” investor might hold 60% stocks, 30% bonds, 10% alternatives/cash. Adjust as goals or markets evolve.

- Reassess your allocation annually—or sooner if your life or the market changes dramatically.

3. Low-Cost Index Funds & ETFs: Simple, Reliable Protection

- Track broad markets with minimal fees—complications and high charges only add risk.

- Choose geographically diversified ETFs and those covering multiple sectors.

- Limit active stock picking, which generally increases volatility and risk for most investors.

4. Dynamic Strategies for Extra Protection

- Stop-Loss Orders: Particularly for active investors, these trigger sales if assets fall to a predefined price.

- Hedging (Options/Futures): Sophisticated investors can use puts, calls, or inverse ETFs to “insure” parts of their portfolio—but mind the complexity and costs.

- Holding Safe-Haven Assets: Allocate part of your funds to gold, high-quality government bonds, or short-maturity deposits/cash equivalents for stability during panic phases.

5. Regular Rebalancing: Stay on Target

- Set a schedule (quarterly or annually) to review and reset your portfolio’s allocation back to its plan.

- Rebalancing enforces discipline—selling high and buying low, the exact opposite of panic behavior.

- Use auto-rebalancing features in many modern investing apps or robo-advisors.

6. Goal-Based Approach: Defeat Emotional Investing

- Define your investment goals (retirement, house, kids’ education, etc.) and time horizon for each.

- Match risk level and asset classes to each goal—short-term needs = safer assets, long-term = growth.

- Stay focused on your targets to avoid knee-jerk, emotion-driven trades in turbulent markets.

7. Use Dollar-Cost Averaging (DCA)

- Invest a fixed amount at regular intervals regardless of asset price—removes the anxiety of “timing the market.”

- This strategy averages out your buying cost and reduces the impact of a sudden crash or spike.

- Automate SIPs (Systematic Investment Plans) in mutual funds or recurring investments in stocks/ETFs.

8. Safe-Haven Assets & Insurance

- Hold a portion of your portfolio in gold, cash, or high-quality bonds to cushion large market swings.

- Consider annuities or insurance products for long-term income and capital protection (especially closer to retirement).

9. Leverage Professional Advice (When Needed)

- Financial advisors can tailor a strategy for your unique needs, managing tax, legal, and emotional pitfalls.

- Robo-advisors offer low-cost, automatically rebalanced portfolios—great for busy investors or those seeking discipline.

10. Avoid the Biggest Mistakes During High Volatility

- Don’t panic sell: Most major sell-offs are followed by strong rebounds—missing recovery days can cost you years of growth.

- Don’t overload on a “hot sector”: Today’s winners could be tomorrow’s laggards.

- Don’t watch the market daily: Long-term investors benefit most from patience, not daily action.

- Don’t ignore tax and transaction costs: Frequent trading can eat into your returns.

FAQs: Protecting Investments from Market Volatility

- Q: Is diversification really necessary?

A: Yes. Even the smartest pros can’t accurately predict next year’s best asset or geography. Diversification is your “insurance.” - Q: Can I protect my crypto or alternative assets?

- A: Only to an extent: keep allocation small, diversify across projects, and use hardware wallets for security. Consider crypto “hedge” products, but understand the risks.

- Q: Should I move to all cash when markets turn?

- A: Sudden moves may leave you out of rebounds—stagger, rebalance, or slowly rotate risk down instead.

- Q: Are there new 2025 tools to help?

- A: Yes! Robo-advisors, auto-rebalance features in apps, and more low-cost ETFs targeting specific risk levels or safe-haven assets.

Case Study: How Diversification and Rebalancing Saved Amit’s Portfolio

Amit, a growth-minded investor, split his wealth across US and Indian equities, government bonds, gold ETFs, and real estate REITs. In a volatile 2022–2024, stocks crashed 30%, but gains in his bond and gold allocation, plus a regular rebalancing routine, meant his overall portfolio dropped only 7%. He avoided panic, stayed consistent, and by 2025 was well ahead of friends who “sold the dip” or relied on a single asset class.

Final Thoughts: Build Resilience, Not Predictions

No one can time the market or dodge every correction—but you can build real resilience. Diversify, keep costs low, automate rebalancing, and adjust risk as life changes. The most successful investors are steady, disciplined, and plan for volatility before it arrives. In 2025, protect your investment portfolio not just for peace of mind, but for real wealth, opportunity, and the freedom to reach your biggest goals.

Strategies to Protect Your Portfolio from Volatility

Comments (3)